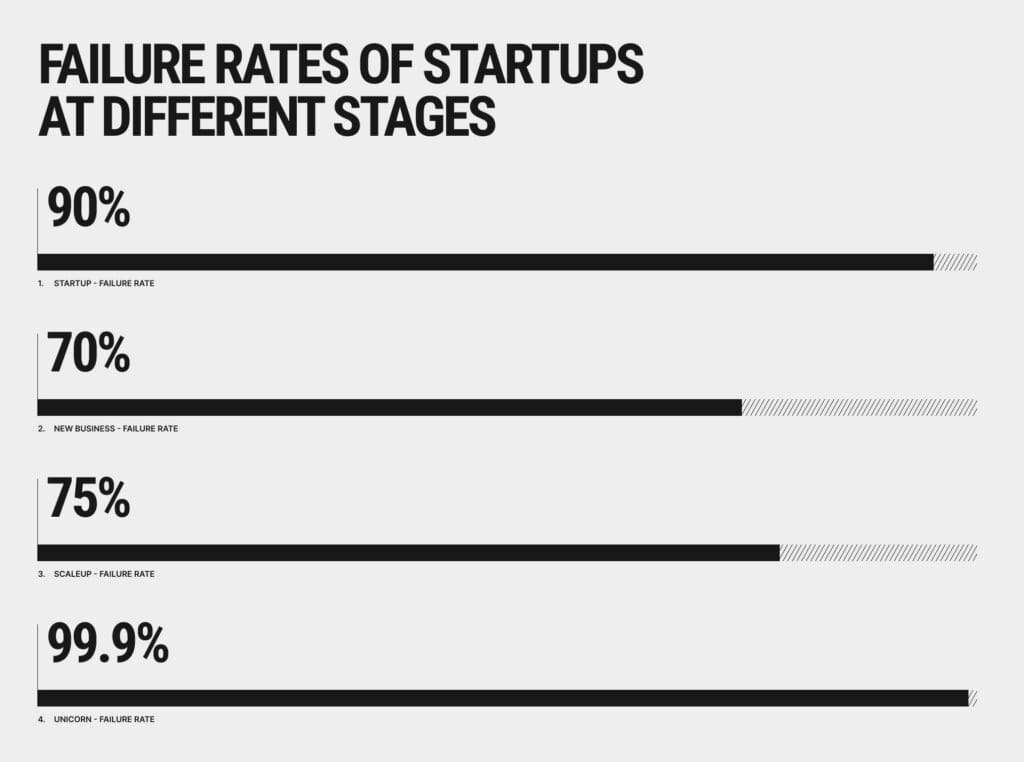

Small startups face daunting odds. In fact, industry analyses estimate that around 90% of new startups eventually fail in the United States. Only about 10% survive beyond the first year. Early failures are common: roughly one in ten new businesses collapses within its first year.

These stark statistics (from U.S. data and global surveys) underscore that most small ventures struggle. As Harvard Professor Tom Eisenmann notes, by his definition, up to 90% of startups don’t make investors money. Understanding why so many small companies fail and learning how to avoid those pitfalls is crucial for aspiring U.S. entrepreneurs and early-stage founders.

A detailed survival charts reveal a steep attrition curve for small U.S. businesses. Bureau of Labor Statistics data show roughly 20% of new businesses fail by the end of their first year, and only about 50% survive five years. (Nearly 70% have failed by year 10.) Small startups, by nature innovative and experimental, often face even higher risks.

After adjusting for high-growth ventures, one report finds 9 out of 10 startups fail. Likewise, fewer than 1 in 5 first-time founders ever build a lasting venture. These data make clear that failure is the norm, not the exception, in the startup world.

In this guide, we examine the most common failure reasons, and strategies for starting and scaling your business successfully.

Startup Failure Rates and Trends

Startup failure is, unfortunately, typical. In a broad overview of U.S. data, one analysis notes that the failure rate for new startups is currently about 90%. Venture-backed technology firms also have grim outcomes: roughly 75% of venture-capital-funded startups never return investors’ capital.

Even with substantial funding, many early-stage tech ventures flame out. For example, the 2019 Startup Genome study famously reported that roughly 90% of all startups fail overall. In the U.S., government statistics (Bureau of Labor) tell a similar story: about 2 in 10 new businesses shut down in their first year, and only about half survive a full five years.

Failures happen for many reasons. ExplodingTopics, a market research site, summarizes that the key drivers of startup failure are “the absence of a product-market fit, poor marketing strategy formulation and implementation, and cash flow problems”.

In other words, entrepreneurs often run into trouble when they build products no one needs, when they fail to reach customers, or when they mismanage finances. Surveyed startup founders echo this: issues with money and runway top the list. A recent founder survey found more than one-third said “running out of money” was a cause of their business’s failure.

Other statistics highlight specific failure factors. Analyses of startup “post-mortems” (founder reports on failed ventures) consistently name “no market need” as the single biggest cause of shutdown. One CB Insights study of 110+ failed startups found that building a solution that didn’t solve a real market problem was cited in 42% of failures.

In practice, this means many small startups die because they solved a problem nobody really had. Financial woes are a close second: about 29% of the failed startups in that analysis ran out of cash. Team issues are also common: about 23% of failures were attributed to having the wrong team or poor leadership.

In summary, the data paint a sobering picture: 9 out of 10 small startups fail by some measure, with most quitting due to product-market misfit, cash crunches, and execution mistakes. The good news is that by studying these patterns, we can learn how to stack the odds in our favor. The next sections delve into the top reasons startups fail and, crucially, how new founders can prevent these problems.

Common Reasons Startups Fail

Startups typically fail for a combination of factors. Here are the most critical pitfalls, each supported by research data:

1. Lack of Product-Market Fit

By far the most frequent killer is building something nobody wants. Startups often “fall in love” with their idea but never validate real customer demand. In CB Insights’ review of failed startup post-mortems, “not targeting a market need” was cited in 42% of failures.

Similarly, other surveys note roughly 34% of failed startups suffered from poor product-market fit. Put, no matter how innovative your tech or service, it must solve a significant pain point. If customers don’t care about the problem you’re solving, the startup will starve for users and revenue.

2. Running Out of Cash

Nearly all startups depend on tight cash flow, especially in early stages. A common pattern is burning capital too fast on development, marketing, or hiring before earning reliable revenue. In CB Insights’ data, 29% of failed startups cited “ran out of money” as a reason. Founders surveyed often agree that lack of funding is the trigger for failure.

It’s not just raising funds that matters, but also how the money is spent. Overspending on lavish offices or features while neglecting core needs can deplete the runway prematurely. Without disciplined budgeting and forecasting, even funded startups can crash once the initial capital is exhausted.

3. Weak or Misaligned Team

A talented, well-rounded team is crucial. Startups often fail because founders lack the necessary skills or co-founder relationships deteriorate. In the CB Insights data, about 23% of failures involved “not the right team”. Poor leadership, internal conflict, or missing expertise (for example, lacking a technical CTO or a business-savvy co-founder) can doom a startup. On the flip side, data suggest that startups with strong founding teams greatly improve their chances.

For instance, startups with a committed co-founder or larger founding team are more likely to attract investment and survive. (One analysis found companies with co-founders had a 163% higher chance of getting growth funding.) Founders should therefore build complementary teams and resolve disputes early, or risk the venture collapsing under poor execution or infighting.

4. Poor Business Model / Planning

Even a good idea can fail if there’s no sustainable plan to make money. Many startups neglect to design a viable revenue model, pricing strategy, or financial plan. According to Startup Genome, 29% of startup failures stemmed from flawed or non-existent business models.

For example, companies might prioritize user growth but never determine how users will pay. Without clear paths to profitability or break-even, a startup may grow the number of users while bleeding money. In practice, failed startups often report they had “no path to reach profitability.” As one expert notes, “Revenue solves all known problems” – if no one pays for the product, eventually investors and founders run out of patience.

Rigorous business planning (with realistic projections) is therefore essential; in fact, 50% of surveyed founders ranked having a strong business plan as top advice for avoiding failure.

5. Poor Marketing and Customer Acquisition

You may have a great product, but if nobody knows about it, you’ll starve. Approximately 22% of failed startups admit they lacked a sound marketing strategy. In today’s digital age, neglecting online marketing, social media, content, and SEO is a major mistake.

The internet offers countless ways to reach customers, and businesses must take advantage. Statista reports that over 4.6 billion people use the internet worldwide, underlining the opportunity. Yet some entrepreneurs skip strategic marketing planning, resulting in products that never find an audience.

Effective startups plan their go-to-market strategy from day one: defining target customers, testing messaging, and allocating a marketing budget. Without ongoing promotion and customer outreach, even well-built products may fail to gain traction.

6. Ignoring Customer Feedback

Startups that don’t listen to users can quickly become irrelevant. Ignoring customer insights or industry shifts can sink a business. Many failed founders later admit they assumed they knew what customers wanted, rather than asking them directly.

In fact, research indicates that startups are twice as likely to succeed when they actively adapt based on customer feedback. Successful startups iterate their product continuously – building a minimum viable product (MVP), gathering user opinions, and making improvements.

By contrast, rigid or “set in stone” founders risk building features no one values. Founders should engage early adopters, run surveys and usability tests, and pivot quickly if demand tells them a new direction is needed. Ignoring the market is a sure path to obsolescence.

7. Scaling Too Quickly

Ironically, growing fast can also cause failure if done prematurely. Many startups mistake growth for success and expand before confirming their foundation. Startup Genome found that about 74% of failed startups scaled prematurely.

Examples include hiring a large team or spending heavily on marketing without first proving product-market fit. Scaling too soon strains resources and creates inefficiencies. If the core product still needs more refinement, rapid expansion increases losses.

Instead, startups should achieve stable traction (steady user growth and revenue) before scaling operations. Controlled growth, adding staff and market reach in measured steps, helps ensure quality and financial stability as you expand.

8. Intense Competition

Entering a crowded market without clear differentiation is risky. Industry data show that about 19% of startup failures are due to being outcompeted. Even well-funded companies can flounder if they lack a unique selling point. For example, Google+, despite massive resources, could not overcome Facebook’s dominance and was shut down.

To survive, startups must research competitors carefully, find a niche or unique angle, and continuously innovate. Failing to stand out often means customers default to better-known alternatives. Startups should analyze market gaps and emphasize what makes them special, whether it’s novel technology, superior user experience, or targeting an underserved segment.

9. External Factors and Other Issues

Finally, some causes are less controllable but still important. Economic downturns, regulatory changes, or unexpected crises (like the COVID-19 pandemic) can derail startups. Rising costs (such as healthcare or rent) and inflation pressure margins. Founders themselves can burn out or lose motivation when progress is slow.

Legal or compliance mistakes, or bad timing (e.g., launching a travel app right before a lockdown) also play roles. While these factors may lie partly outside their control, smart founders monitor the environment and build flexibility into their plans. For instance, having contingency funds or the ability to pivot business models can mitigate external shocks.

Each of the above reasons often overlaps with others. For instance, a cash crunch may result from poor marketing or a flawed business model, and team problems can exacerbate any challenge. By recognizing these common failure patterns, validated by data and real startup stories, entrepreneurs can take proactive steps to avoid them.

How to Avoid Failure: Best Practices for Startups

While startup challenges are real, there are proven strategies to improve your odds. Below are key recommendations, grounded in data and expert advice, to help aspiring founders start and scale more successfully:

1. Validate Your Idea First

Before coding features or manufacturing products, validate market demand. Talk to potential customers, run surveys, and launch a minimum viable product (MVP) to test assumptions. Experts advise founders to confirm desirability, feasibility, and viability early.

For example, use letters of intent or early signup pledges as experiments. Validating early ensures you’re solving a real problem: remember that 42% of startups fail for lack of need. If early feedback is weak, consider pivoting the concept or adjusting the target market.

The lean startup methodology emphasizes “build-measure-learn” loops to find product-market fit before fully scaling. In short: don’t build in a vacuum. Use data and customer conversations to refine your product until users are genuinely excited about it.

2. Keep a Lean Budget and Manage Cash

Plan your finances meticulously. Create realistic burn-rate and revenue projections, and conserve cash until you have proven revenue. Lean budgeting means prioritizing essential expenses: focus on product development and customer acquisition rather than luxury offices or unnecessary hires.

A well-structured financial plan includes setting a clear break-even target and tracking runway (how long funds will last) at every stage. According to entrepreneurs surveyed, having “more financial backing” is key advice to avoid failure. If possible, raise enough to reach profitability (as Wilbur Labs emphasizes, “Revenue solves all known problems”). Even after fundraising, spend carefully.

Use key performance indicators (KPIs) to monitor cash flow, and be ready to cut costs if growth stalls. Many successful founders recommend “bootstrapping” in early phases – funding the startup with personal or customer money to maximize discipline, before chasing big funding rounds.

3. Build a Strong, Complementary Team

Surround yourself with people who fill your skill gaps. Seek co-founders or early hires who bring technical expertise, industry knowledge, or business acumen that you lack. Ensure everyone shares the vision and work ethic. Use formal or informal tools (like founder agreements and regular team check-ins) to set expectations and resolve conflicts early.

Consider advisors or mentors who can guide inexperienced founders. The Wilbur Labs survey found that founders often regret missing co-founders or mentors, and agreed that hiring the right team is vital to survival. In practice, successful startups invest heavily in culture and communication.

They also hire slowly and fire fast, meaning they take care in recruitment, but do not hesitate to remove team members who aren’t a fit. A cohesive team can navigate challenges together; lacking one makes overcoming obstacles exponentially harder.

4. Develop a Solid Business Model

From day one, be clear on how the startup will make money. Test and iterate revenue models early: subscriptions, licensing, transaction fees, ads, or other streams. Don’t rely solely on raising future funding as a plan. Instead, focus on strategies for customer monetization from the start. Treat metrics like customer lifetime value (LTV) and customer acquisition cost (CAC) as critical data points.

Avoid unsustainable pricing or giveaways: learn from failures like MoviePass (which collapsed under a free-for-all pricing model). Involve early investors or business mentors in reviewing your financial model. If initial targets seem out of reach, consider adjusting features, costs, or markets before growing further.

Remember, about 29% of startups fail because they had no viable business plan. A strong business plan – covering revenue, expenses, and break-even analysis – will guide decisions and reassure stakeholders that the company can survive.

4. Plan and Execute a Marketing Strategy

Marketing is not optional; it’s essential from the first day. Define your target audience in detail, then craft a marketing plan that reaches them effectively. This might include content marketing (blogs, social media, SEO), paid ads, partnerships, or public relations. Even on a small budget, focus on high-leverage channels (for example, niche online communities or local events for a local startup).

Continuously measure marketing results and optimize campaigns. According to small business surveys, a surprising number of founders admit they underinvest in marketing or don’t understand it. To avoid this pitfall, allocate sufficient budget and attention to marketing tasks as if they were product development tasks.

Bring in advisors or agencies if needed, especially early on, to build brand awareness and credibility. Solving a problem matters little if potential customers never hear about your solution.

5. Listen and Adapt to Customers

Once your product is in the hands of users, listen to what they say. Proactively solicit feedback through surveys, user tests, and analytics. Please pay attention to usage data and customer support tickets to see where users struggle or what features they value. Use this insight to refine your offering. In the best startups, customer feedback drives product pivots and feature changes.

For instance, there are many cases where founders discovered their customers actually wanted something slightly different than planned, and pivoting early saved the business. As noted earlier, startups that adapt based on insights are about twice as likely to survive.

Establish formal processes (like weekly review of customer feedback, sprint retrospectives, etc.) so that listening becomes part of your culture. Remember: building a “unicorn” often means being obsessed with the problem from the customer’s perspective, not clinging stubbornly to your original solution.

6. Grow Carefully, Don’t Scale Prematurely

Scaling should be deliberate. Before hiring at a frenzy or exploding marketing spend, ensure your product has market traction. Use metrics such as consistent month-over-month user growth or revenue to gauge readiness. Aim for a solid, repeatable sales/marketing engine before taking on major expansion.

For example, instead of opening offices in five cities at once, pilot in one market, learn the local challenges, then copy that model gradually. Many founders regret expanding too quickly; in one study, about three-quarters of failed startups had scaled too soon.

The key is to match the growth pace to the learning pace. As a rule of thumb, only add new hires or locations when you have the processes to onboard them effectively.

7. Monitor Competition and Market Trends

Keep an eye on competitors and industry shifts. Study what similar companies are doing and how customers respond. Seek to differentiate: it could be through better technology, exceptional customer service, a unique branding angle, or targeting an underserved segment. If a giant competitor launches a similar feature, be ready to quickly iterate (for example, by focusing on niches or open marketing).

Cultivate an innovation mindset: what features, partnerships, or business lines can you develop that others are overlooking? Strategic flexibility helps: if a competitor moves in on one product line, you may shift focus or improve your offering faster.

While you can’t always win a direct fight with a multi-billion-dollar incumbent, you can often succeed by “playing different” – for example, selling to a market segment they ignore, or combining your product with an innovative service.

8. Plan for Risks and Legal Issues

Protect your business by anticipating potential pitfalls. Make sure all legal and regulatory bases are covered: obtain necessary licenses, understand intellectual property rules, and comply with tax laws. Even small oversights (like not registering a trademark or misclassifying employees) can lead to expensive trouble.

Set up basic corporate governance: clear shareholder or partnership agreements, simple accounting and banking, and proper legal structure (LLC, C-corp, etc.). These may seem like overhead, but they prevent disruption later. Also, consider insurance (liability, cyber, etc.) if your industry is high-risk.

Finally, keep an eye on the economic climate: if interest rates rise or funding tightens, have contingency plans (e.g., cost-cutting or alternate funding routes) ready. Being prepared for “what-if” scenarios can keep a startup afloat when conditions change suddenly.

9. Stay Resilient and Keep Learning

On a personal level, founders must stay mentally and physically fit. Startup life is stressful, and long hours can lead to burnout (which has sunk roughly 8% of startups per CB Insights data). Take care of yourself and delegate when needed. Learn from every setback: Many successful entrepreneurs started companies that initially failed.

As one study of founders showed, those who had previous failures actually had a higher success rate later on. Cultivate a growth mindset: treat failures as lessons. Keep reading, seeking mentors, and networking with other founders. This ongoing learning will help you spot problems early and pivot intelligently.

Each startup’s journey is unique, but these strategies form a strong foundation. They directly address the documented causes of failure: ensuring real market demand, sound finances, capable teams, and adaptable execution. By applying these best practices, validating ideas early, planning carefully, engaging customers, and staying flexible help entrepreneurs give their startups the best chance to survive and thrive.

Conclusion

The data are clear: most small startups do not survive. But this knowledge is not meant to discourage; rather, it equips aspiring founders with actionable insights. By studying why startups fail, entrepreneurs can spot red flags and take preventive measures.

A well-planned, validated business with a great team and strong market fit can beat the odds. Armed with a thorough understanding of failure patterns and a playbook of solutions, founders can navigate challenges, avoid common pitfalls, and build sustainable businesses.

Startups do succeed when founders learn from failures and execute rigorously. As the experts advise, focus on real customer problems, stay lean, test your assumptions, and adapt as you grow. With these strategies, backed by data and proven in the field, small startups can improve their survival rates and turn bold ideas into lasting ventures.

Also Read: Growth Hacking Guide For A Small Business